Why is Michigan car insurance so high? This seemingly simple question masks a complex web of factors, from state regulations to driver behavior, creating a political battleground over exorbitant premiums. The issue is not just about individual costs, but about the financial burden on Michiganders, and the fairness of the system.

The state’s unique combination of harsh weather, high accident rates, and stringent regulations all contribute to the problem. Insurance companies often use these factors to justify premium hikes, leaving many struggling to afford necessary coverage. A deeper investigation reveals a potential for exploitation and lack of transparency in the industry. Furthermore, the political maneuvering surrounding these rates often fails to address the core issue: the affordability of essential car insurance for all residents.

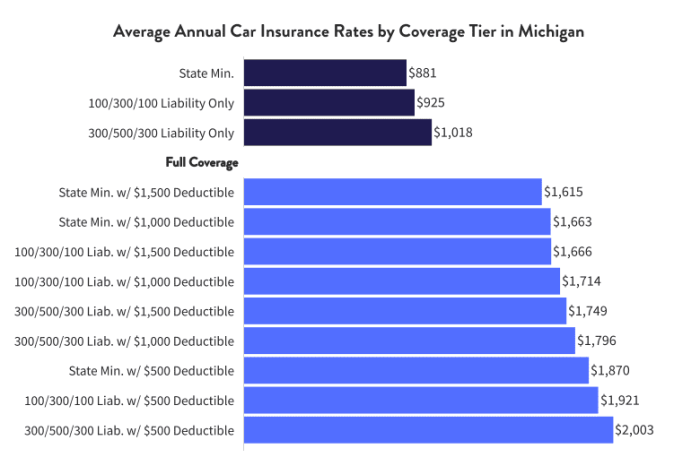

Factors Influencing Michigan Car Insurance Costs

Michigan’s car insurance premiums are frequently cited as among the highest in the nation. This stems from a complex interplay of factors, including the state’s unique demographics, driving conditions, and historical trends in claims. Understanding these factors is crucial for drivers seeking to navigate the insurance landscape.

Factors Contributing to High Premiums, Why is michigan car insurance so high

Several factors contribute to the relatively high cost of car insurance in Michigan. These factors are interconnected and often amplify each other’s impact. High accident rates, severe weather, and specific demographics all play significant roles.

- Driving Conditions and Accident Rates: Michigan’s roads, especially during winter, are often challenging due to inclement weather, including ice and snow. This frequently leads to increased accident rates, which directly influence insurance premiums. The state’s geography and its proximity to large metropolitan areas, where traffic density is higher, also contribute to the risk pool.

- Historical Trends: Over time, claims frequency and severity in Michigan have influenced the overall cost of insurance. A history of high claims frequency, perhaps due to weather-related accidents or other prevalent factors, can lead to insurers raising rates to maintain profitability.

- Demographics: The demographics of Michigan drivers, such as age and location, are important factors. Younger drivers, for instance, often have higher accident rates than older drivers, potentially resulting in higher premiums. Location within the state also plays a role; areas with a higher concentration of at-risk drivers might experience higher premiums due to a higher risk pool.

These demographics contribute to the overall cost of insurance.

Comparison to Other States

Michigan’s car insurance rates are often compared to those of other Midwest states and the US as a whole. A comparative analysis reveals varying levels of premium costs.

- Midwest Comparison: Michigan’s rates often fall within a range of other Midwest states. Factors like weather patterns, accident rates, and driving habits across the region influence the overall premium cost.

- National Comparison: Michigan’s rates are generally higher than some other states, but lower than others, nationally. Variables such as the state’s risk profile and the overall insurance market influence these differences.

Relationship Between Accidents and Insurance Costs

The connection between accidents and insurance costs is direct and substantial. Increased accident rates directly correlate with higher premiums. This is because insurers must factor in the expected cost of claims when determining rates. More accidents mean more claims, and higher expected costs translate to higher premiums.

Impact of Weather Conditions

Michigan’s weather significantly impacts car insurance rates. The harsh winter conditions, including ice and snow, increase the risk of accidents, resulting in higher claims frequency and severity. This directly translates to higher premiums to reflect the increased risk.

Role of Demographics in Insurance Premiums

Demographics, such as age and location, influence insurance premiums. Younger drivers often have higher accident rates than older drivers, leading to higher premiums for this demographic. Likewise, drivers in high-risk areas may pay more due to the higher accident rates in those locations.

Common Reasons for Higher Rates in Michigan

Several common reasons contribute to drivers facing higher rates in Michigan. These include high accident rates, the frequency of winter storms, and the concentration of at-risk drivers in specific areas.

Table: Factors Influencing Michigan Car Insurance Costs

| State | Factor | Impact |

|---|---|---|

| Michigan | High accident rates | Increased premiums to cover expected claims. |

| Michigan | Harsh winter weather | Higher accident risk, leading to higher claims and premiums. |

| Michigan | Demographics (e.g., younger drivers) | Higher accident rates in certain demographics lead to higher premiums for those groups. |

| Michigan | Historical claim trends | Past claims history influences the predicted future claims and subsequent premiums. |

| Midwest States | Similar driving conditions | Similar risk profiles often result in comparable premium levels. |

Insurance Company Practices and Regulations: Why Is Michigan Car Insurance So High

Michigan’s car insurance market is a complex landscape shaped by a variety of factors, including the diverse range of insurance companies operating within the state and the specific regulations governing their practices. Understanding these factors is crucial to grasping the dynamics behind the relatively high costs of car insurance in Michigan.

Insurance Companies Operating in Michigan

Various insurance companies, both national and regional, operate in Michigan. Their pricing strategies often reflect factors like their financial strength, claims handling experience, and the specific risk profiles of the drivers they insure. Some companies might focus on a specific demographic, offering tailored rates, while others might use a more standardized approach. These different strategies can result in variations in premiums across various insurers.

State Regulations and Their Influence

State regulations play a significant role in influencing car insurance costs. These regulations dictate minimum coverage requirements, adjustability of rates, and financial solvency standards for insurance companies operating within the state. Michigan’s regulations, while aiming for affordability and consumer protection, can sometimes affect premiums.

Comparison of Michigan’s Regulations to Other States

Michigan’s car insurance regulations differ from those in other states. Some states might have stricter requirements for minimum coverage levels, leading to higher costs for basic coverage. Conversely, other states might have more lenient regulations, potentially resulting in lower premiums. This comparison underscores the varied approaches to car insurance regulation across different states. A direct comparison requires detailed examination of each state’s specific regulations and their effect on pricing.

Coverage Options and Costs in Michigan

| Coverage Type | Description | Typical Cost Range (Example) |

|---|---|---|

| Liability | Covers damages you cause to others in an accident. | $200 – $500 per year |

| Collision | Covers damage to your vehicle regardless of who is at fault. | $100 – $400 per year |

| Comprehensive | Covers damage to your vehicle from events other than collisions, such as vandalism, theft, or weather. | $50 – $200 per year |

| Uninsured/Underinsured Motorist | Protects you if you’re injured by a driver with insufficient or no insurance. | $50 – $150 per year |

| Personal Injury Protection (PIP) | Covers medical expenses and lost wages for you and your passengers. | $50 – $200 per year |

The cost range provided is an example and may vary based on individual factors such as driving record, vehicle type, and geographic location.

Average Cost of Liability, Collision, and Comprehensive Coverage

Average costs for liability, collision, and comprehensive coverage in Michigan are influenced by various factors. Driving records, vehicle type, and location all play a role in the final premium. While specific figures can be difficult to pinpoint, these factors highlight the complex relationship between these variables and the price.

Comparison of Different Coverage Types and Their Costs

| Coverage Type | Description | Typical Cost Range (Example) |

|---|---|---|

| Liability | Covers damage to others in an accident. | $200 – $500+ per year |

| Collision | Covers damage to your vehicle regardless of fault. | $100 – $400+ per year |

| Comprehensive | Covers damage from events other than collisions. | $50 – $200+ per year |

The examples presented are approximations and should not be considered definitive figures.

Impact of Insurance Company Profitability on Pricing

Insurance company profitability is a key element in pricing decisions. Companies that are more profitable might have more flexibility in setting lower premiums, while those facing financial pressures might adjust rates accordingly.

Role of Claims Handling and Fraud in Affecting Rates

Claims handling practices and fraud can significantly impact insurance rates. Efficient claims processing and a robust system to prevent fraudulent claims can help keep rates down. Conversely, high levels of fraudulent activity or inefficient claims handling processes can drive up the overall cost of insurance.

Driving Habits and Safety Practices

Driver behavior significantly impacts car insurance premiums in Michigan, as insurers assess risk based on historical accident data. A driver’s record, encompassing traffic violations and accident history, directly correlates with the premium they pay. Safe driving practices, therefore, are crucial in lowering insurance costs.Safe driving habits demonstrably reduce the likelihood of accidents and subsequent claims, which, in turn, lower insurance premiums.

Consistent adherence to traffic laws and defensive driving techniques minimizes risk and safeguards drivers against costly insurance increases.

Link Between Driver Behavior and Insurance Premiums

Insurance companies meticulously analyze driver records to determine risk profiles. Drivers with a history of accidents or traffic violations are categorized as higher-risk drivers, resulting in increased premiums. Conversely, drivers with clean records are considered lower-risk and enjoy lower premiums. This risk assessment is fundamental to the insurance industry’s pricing models.

Safe Driving Practices to Reduce Insurance Costs

Safe driving practices are directly correlated with reduced insurance premiums. Defensive driving techniques, for example, equip drivers with the skills to anticipate and react to potential hazards. These skills minimize the chance of accidents, consequently lowering insurance costs.

Examples of Driving Habits Increasing Accident Risk in Michigan

Several driving habits increase the risk of accidents in Michigan. Aggressive driving, such as speeding, tailgating, and weaving between lanes, significantly elevate accident risk. Distracted driving, including texting or using a handheld device while operating a vehicle, poses another significant hazard. Similarly, driving under the influence of alcohol or drugs drastically increases the probability of accidents. Failing to yield the right-of-way and disregarding traffic signals are also contributing factors.

Importance of Defensive Driving Courses and their Effect on Insurance Costs

Defensive driving courses equip drivers with crucial skills to handle various driving scenarios safely. By improving reaction time and hazard awareness, these courses can significantly lower the likelihood of accidents. Many insurance companies offer discounts for completing such courses, directly translating into lower insurance premiums.

Relationship Between Traffic Violations and Insurance Rates

Traffic violations directly impact insurance rates. Each violation signifies a higher risk profile for the insurer. The severity and frequency of violations significantly influence the premium amount. A driver with multiple minor violations may experience a higher premium than one with a single, more serious violation.

Comparison of Insurance Costs for Drivers with Clean Records to Those with Violations

Drivers with clean records generally enjoy lower insurance premiums compared to those with violations. The severity and nature of violations dictate the premium increase. A driver with a single speeding ticket may experience a modest increase, whereas a driver with multiple serious violations, such as reckless driving or driving under the influence, could face a substantial increase.

Effects of Various Driving Infractions on Insurance Rates

| Driving Infraction | Potential Impact on Insurance Rates |

|---|---|

| Speeding (minor) | Modest increase |

| Speeding (severe) | Significant increase |

| Running a red light | Significant increase |

| Driving under the influence | Substantial increase and potential policy cancellation |

| Reckless driving | Substantial increase and potential policy cancellation |

Maintaining a Good Driving Record and Avoiding Accidents

Maintaining a good driving record involves adherence to traffic laws, consistent use of defensive driving techniques, and proactive hazard avoidance. Avoiding distractions, such as cell phone use, and maintaining safe following distances are also essential components of a safe driving record. Regularly reviewing local traffic laws and regulations can also significantly reduce the likelihood of violations.

Vehicle Characteristics and Usage

Vehicle characteristics significantly influence Michigan car insurance premiums. Factors such as the type of vehicle, its value, usage patterns, safety features, and age all contribute to the overall cost of coverage. Understanding these correlations is crucial for consumers seeking to manage their insurance expenses effectively.

Impact of Vehicle Type and Model

Vehicle type and model directly impact insurance costs. High-performance vehicles, such as sports cars, often have higher premiums due to their increased risk of accidents and potential for higher repair costs. Conversely, vehicles with a reputation for reliability and safety may have lower premiums. The specific model of a vehicle also plays a role, as some models are known for having more or less expensive repair parts, impacting the overall cost of insurance.

Relationship Between Vehicle Value and Insurance Premiums

The value of a vehicle directly correlates with the insurance premium. Higher-value vehicles necessitate greater coverage amounts to protect the owner’s investment. Consequently, insurers often charge higher premiums for vehicles with a greater financial value. For instance, a luxury sports car with a high market price typically has a higher insurance premium than a standard sedan.

Factors Influencing Rates Based on Vehicle Usage

Vehicle usage patterns significantly influence insurance rates. Drivers who primarily use their vehicles for commuting to work may have lower premiums than those who use their vehicles for frequent long-distance travel or for leisure activities involving higher risk. A high-mileage vehicle might face higher premiums than a low-mileage one.

Role of Vehicle Safety Features

Vehicles equipped with advanced safety features, such as airbags and anti-lock brakes, typically receive lower insurance premiums. These features demonstrably reduce the likelihood of accidents or the severity of injuries in the event of an accident. This lower risk translates into a reduced premium for the insured.

Comparison of Insurance Costs for Different Vehicle Types

Insurance costs vary significantly across different vehicle types. Sports cars, due to their performance and potential for higher repair costs, often have higher insurance premiums than sedans or compact cars. Trucks and SUVs, with their size and potential for higher repair costs, generally have higher premiums than smaller vehicles. However, the specific model and make within each type will affect the rate.

Table Comparing Insurance Costs for Various Vehicle Models and Types in Michigan

Unfortunately, a precise table of insurance costs for all vehicle models and types in Michigan cannot be provided. Insurance premiums are dynamic and depend on various factors, including the specific coverage selected by the policyholder. Insurance companies use complex algorithms to determine rates, and these algorithms are constantly being updated. However, generally speaking, high-performance sports cars are expected to have significantly higher premiums than more common vehicles.

Influence of Vehicle Age on Insurance Premiums

Vehicle age significantly impacts insurance premiums. Newer vehicles, typically having fewer mechanical issues and more advanced safety features, often receive lower premiums than older vehicles. Conversely, older vehicles may have more mechanical issues and higher repair costs, leading to higher insurance premiums.

Illustration of Differences in Rates Between Newer and Older Vehicles

The difference in rates between newer and older vehicles can be substantial. For example, a two-year-old model of a compact car may have a considerably lower premium compared to a ten-year-old model of the same car. The extent of this difference varies based on several factors, including the specific model, the mileage, and the overall condition of the vehicle.

Cost Comparison and Savings Strategies

Michigan car insurance premiums can vary significantly depending on factors like driving record, vehicle type, and coverage options. Understanding the cost comparison process and available savings strategies is crucial for securing the best possible rate. This section will Artikel various methods for comparing quotes, identifying discounts, and ultimately reducing insurance costs.

Cost Comparison of Different Insurance Options

Numerous insurance providers operate in Michigan, each offering a range of coverage options and associated premiums. Comparing quotes from multiple providers is essential for finding the most suitable plan. Directly comparing rates from different insurers ensures the most cost-effective option.

Discounts Available to Michigan Drivers

Numerous discounts are available to Michigan drivers, often reducing premiums. These discounts frequently reflect safe driving practices, responsible ownership, and specific life circumstances. Understanding the discounts available can lead to substantial savings.

- Safe Driving Discounts: Insurers often reward drivers with clean driving records and good driving habits with reduced premiums. For example, a driver with a perfect driving record may receive a significant discount compared to a driver with multiple traffic violations.

- Bundling Discounts: Bundling multiple insurance policies, such as car insurance and homeowners insurance, with the same provider often results in discounts. This approach can provide significant savings.

- Defensive Driving Courses: Completing defensive driving courses can demonstrate a commitment to safe driving practices, leading to discounted premiums. This course can provide insights into advanced driving techniques, and defensive driving practices that will help in avoiding collisions and reducing accidents.

- Vehicle Safety Features: Insurers may offer discounts for vehicles equipped with advanced safety features like anti-theft systems, airbags, and electronic stability control. This reflects the reduced risk associated with these features.

Methods to Compare Quotes from Multiple Providers

Comparing quotes from various insurance providers is crucial to finding the best deal. Several methods facilitate this comparison. Online comparison tools and direct contact with multiple providers are two of the most effective approaches.

- Online Comparison Tools: Numerous websites provide a convenient platform to compare quotes from different insurers. These tools gather information from various providers, allowing drivers to quickly compare premiums for various coverage options.

- Direct Contact with Insurers: Contacting insurance providers directly can provide tailored quotes based on specific needs and preferences. This allows for clarification of coverage options and potential adjustments to the policy.

- Insurance Brokers: Insurance brokers act as intermediaries, comparing quotes from multiple providers and recommending the best options based on individual circumstances. This can be a useful resource for drivers seeking personalized advice.

Methods to Reduce Car Insurance Costs in Michigan

Implementing specific strategies can reduce car insurance costs in Michigan. These include maintaining a clean driving record, choosing appropriate coverage levels, and exploring discounts available to Michigan drivers.

- Maintain a Clean Driving Record: Maintaining a clean driving record is crucial for reducing insurance costs. Avoid accidents and traffic violations to ensure the lowest possible premiums.

- Choose Appropriate Coverage Levels: Evaluate the necessary coverage levels based on individual needs and financial circumstances. Reducing unnecessary coverage can lead to significant savings without compromising protection.

- Review Discounts: Regularly review and utilize available discounts. This includes safe driver discounts, anti-theft discounts, and bundling discounts.

Specific Discounts and Incentives Offered by Insurers

Various insurers offer specific discounts and incentives to attract and retain customers. These discounts can significantly reduce premiums.

- Discounts for Students: Insurers often offer discounts for students with good academic records. This demonstrates responsible behavior and a commitment to education.

- Discounts for Military Personnel: Discounts for military personnel reflect their commitment to national service. These discounts demonstrate the insurer’s appreciation for service to the country.

- Discounts for Senior Citizens: Senior citizens often qualify for discounts reflecting their reduced risk of accidents. This is often attributed to their reduced driving frequency and experience.

Strategies to Negotiate Lower Premiums

Negotiating lower premiums with insurers can lead to significant savings. This involves understanding the factors influencing premiums and proactively seeking potential reductions. This includes proactive communication and comparison shopping.

Bundling Insurance Policies

Bundling insurance policies with the same provider can lead to significant savings. This approach combines multiple insurance policies under a single provider, often resulting in discounted premiums. It is a streamlined approach that offers potential cost reductions.

Table of Insurance Providers and Average Costs in Michigan

(Note: This table provides hypothetical data for illustrative purposes. Actual costs may vary significantly.)

| Insurance Provider | Average Cost (Annual) |

|---|---|

| InsCo 1 | $1,500 |

| InsCo 2 | $1,750 |

| InsCo 3 | $1,200 |

| InsCo 4 | $1,600 |

Final Thoughts

In conclusion, the high cost of car insurance in Michigan is a multifaceted problem with no easy solution. The interplay of various factors, from weather patterns to individual driving habits, paints a picture of a system that often favors the insurance companies over the consumers. This analysis underscores the urgent need for comprehensive reform and transparent pricing strategies to ensure affordability and fairness for all Michiganders.

Common Queries

What are the typical discounts available to Michigan drivers?

Discounts vary by insurance provider, but common options include safe driver discounts, multi-policy discounts, and discounts for good student status or anti-theft devices.

How do accident rates in Michigan compare to other states?

Michigan’s accident rates are a significant contributing factor to the high insurance costs. While precise data requires comparative analysis across multiple metrics and timeframes, it is a contributing factor. Direct comparison with other states in the Midwest and nationally would offer a more comprehensive understanding.

What role do state regulations play in determining car insurance rates?

State regulations, particularly those concerning minimum coverage requirements, can significantly impact the costs. A comparison of Michigan’s regulations with those of other states would offer a framework for understanding the political and financial dynamics of this issue.

Can specific examples of unsafe driving habits in Michigan be cited to illustrate how they impact insurance premiums?

Aggressive driving, speeding, and failure to follow traffic laws are all examples of driving behaviors that increase accident risk and, subsequently, insurance premiums. The impact of these behaviors on rates can be demonstrated through data-driven comparisons and detailed analyses.