I can’t afford car insurance. This pressing issue affects many, creating financial strain and raising important questions about accessibility and affordability. The high cost of insurance, coupled with low income, can leave people vulnerable to significant financial penalties and legal ramifications. This discussion will explore various solutions, alternatives, and coverage options to navigate this challenge.

This guide provides a comprehensive overview of the factors contributing to the inability to afford car insurance. It explores strategies to reduce costs, examines government assistance programs, and compares various insurance options. Ultimately, it aims to equip readers with practical steps to find affordable coverage that meets their individual needs.

Understanding the Problem

The rising cost of car insurance presents a significant financial hardship for many individuals and families. This issue is particularly acute for those with limited financial resources, who often face a difficult choice between essential needs and the necessity of maintaining vehicle insurance. The consequences of not having adequate coverage extend beyond the financial, potentially impacting personal safety and legal standing.

This section delves into the multifaceted nature of this problem, examining its contributing factors, potential ramifications, and the complexities of various insurance options.The financial burden of car insurance can be substantial, particularly when premiums are high and income is low. This disparity creates a significant barrier to entry, making it challenging for individuals and families to afford the protection they need.

Furthermore, limited access to affordable coverage options can exacerbate the problem, leaving those struggling with limited choices.

Financial Hardship Associated with Car Insurance

Affordability of car insurance is often a critical challenge for individuals with lower incomes. High premiums, frequently exceeding the financial capacity of low-income individuals, pose a significant hurdle. The financial burden of unexpected vehicle repairs or accidents can be catastrophic, and without adequate insurance, individuals are left vulnerable to substantial financial losses. This often results in individuals delaying or forgoing necessary maintenance, leading to a higher risk of more expensive repairs and accidents in the future.

Limited access to affordable coverage options further exacerbates this issue.

Factors Contributing to Inability to Afford Car Insurance

Several factors contribute to the difficulty many face in obtaining and maintaining car insurance. Low income is a significant factor, as insurance premiums often exceed the financial capacity of those with limited resources. High premiums, a consequence of factors like geographic location, driving history, and vehicle type, further contribute to this problem. Limited access to affordable coverage options, such as specialized discounts or different coverage levels, can also hinder individuals from obtaining suitable protection.

Consequences of Not Having Car Insurance, I can’t afford car insurance

The consequences of not having car insurance can be severe, extending beyond financial penalties to encompass potential legal ramifications. Failure to maintain insurance can result in significant financial penalties, including hefty fines and potential suspension of driving privileges. Furthermore, the lack of coverage leaves individuals vulnerable to legal action in the event of an accident. In many jurisdictions, uninsured drivers face legal liability and potentially crippling financial responsibility for damages incurred.

Types of Car Insurance Coverage and Their Costs

Various types of car insurance coverage are available, each with different levels of protection and associated costs. These include liability coverage, which protects against damages to others in the event of an accident, and comprehensive coverage, which provides protection against a wider range of events such as vandalism or theft. Collision coverage, protecting against damages to the insured vehicle in an accident, also falls under this category.

The costs of these coverages vary significantly based on factors such as the driver’s history, vehicle type, and location.

Comparison of Insurance Levels and Deductibles

| Coverage Level | Description | Example Cost (Annual) |

|---|---|---|

| Liability Only | Covers damages to others in an accident. | $500 – $1500 |

| Liability + Collision | Covers damages to the insured vehicle and to others in an accident. | $1000 – $2500 |

| Liability + Collision + Comprehensive | Covers damages to the insured vehicle, to others in an accident, and various events such as vandalism or theft. | $1500 – $3500 |

Note: Costs are examples and may vary significantly based on individual circumstances. Deductibles, the amount the insured must pay out-of-pocket before insurance coverage applies, further impact the overall cost of coverage. Higher deductibles typically lead to lower premiums, but the insured bears more responsibility in the event of a claim.

Exploring Solutions

Reducing car insurance costs requires a multifaceted approach, considering various factors that influence premiums. This section details strategies to lower insurance expenses, focusing on responsible financial management, credit improvement, and exploring affordable insurance options. Ultimately, the goal is to find a balance between responsible driving and maintaining an affordable insurance plan.Finding affordable car insurance involves understanding the intricate relationship between various factors.

These factors range from driving history and vehicle type to creditworthiness and location. By analyzing these elements and implementing appropriate strategies, individuals can significantly reduce their insurance costs.

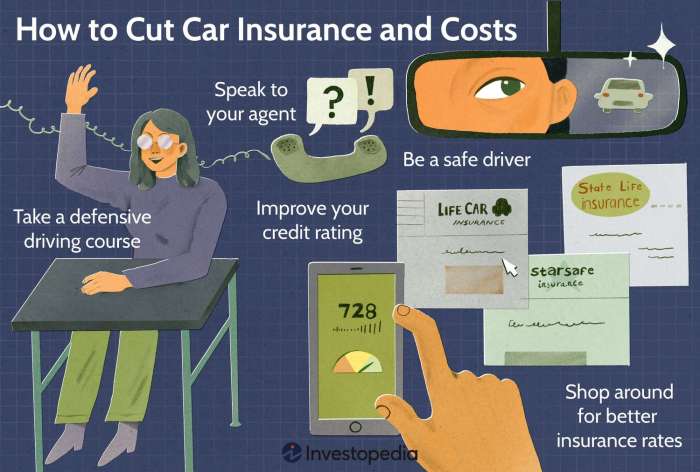

Strategies for Reducing Car Insurance Costs

Understanding the factors influencing car insurance premiums is crucial for identifying cost-saving strategies. Careful consideration of driving habits, vehicle type, and location can significantly impact the final premium.

- Safe Driving Practices: Maintaining a clean driving record is paramount. Avoiding accidents and traffic violations directly impacts insurance premiums. Defensive driving courses can enhance safe driving skills and potentially reduce premiums. Studies have shown that drivers with clean records tend to pay lower premiums.

- Vehicle Selection: Certain vehicle types are more prone to damage or theft, leading to higher insurance costs. Choosing a vehicle with safety features and a lower risk profile can result in a more affordable policy. For example, a newer model car with advanced safety features might have lower premiums compared to an older model with fewer safety features.

- Insurance Discounts: Numerous discounts are available from various insurance providers. These discounts often relate to factors like vehicle anti-theft features, good student status, and safe driving practices. Drivers should explore available discounts to reduce premiums.

- Bundling Policies: Bundling multiple insurance policies, such as home and auto, can sometimes lead to discounts. This is because insurers may see bundling as a lower risk and reward the customer with a reduced premium.

Improving Credit Scores and their Impact

Creditworthiness significantly influences car insurance premiums. A higher credit score often translates to a lower premium. This is because insurers consider credit scores as a measure of financial responsibility and risk.

- Understanding Credit Scores: A credit score is a numerical representation of an individual’s creditworthiness, calculated based on credit history. A higher score typically indicates responsible financial habits. Factors like timely payments, low debt levels, and a history of responsible credit utilization contribute to a higher score.

- Improving Credit Score: Improving credit scores can be achieved through consistent on-time payments, managing existing debts responsibly, and avoiding new credit applications without a solid need. Regular monitoring and proactive management of credit reports are vital.

- Impact on Insurance Premiums: Insurers often use credit scores as a key factor in determining premiums. A higher credit score can lead to a significant reduction in premiums, whereas a lower score may result in higher premiums.

Finding Affordable Insurance Providers

Exploring various insurance providers is essential to identify affordable options. Comparing quotes from different companies is crucial to finding the best deal.

- Comparing Quotes: Utilizing online comparison tools or contacting multiple insurance providers directly can help in comparing quotes. This process allows for a clear understanding of different policy options and pricing structures. Comparison tools typically provide an overview of various insurance providers’ rates and policies, which can help individuals make informed decisions.

- Negotiating Rates: Directly contacting insurance providers can provide opportunities for negotiation and potentially lower premiums. This process may involve presenting your circumstances and emphasizing factors that qualify for discounts. This is particularly beneficial when negotiating rates with the insurance provider.

- Evaluating Policy Coverage: Evaluating policy coverage is critical to ensuring that the chosen policy meets the specific needs of the individual. This includes coverage amounts, deductibles, and specific types of coverage to be included.

Government Assistance Programs for Low-Income Individuals

Several government assistance programs can aid low-income individuals in securing affordable car insurance. These programs often provide subsidies or reduced premiums.

- Eligibility Criteria: Eligibility for these programs often depends on factors like income, employment status, and household size. Understanding the specific criteria for each program is essential to determine if an individual qualifies.

- Application Process: The application process varies depending on the specific program. Individuals should research the application requirements and procedures. This involves determining the necessary documents and the steps required to complete the application process.

- Impact on Insurance Costs: These programs can significantly reduce car insurance costs for low-income individuals, making car insurance more accessible and affordable.

Insurance Company Cost Structures

Understanding the cost structures of different insurance companies can help individuals make informed decisions. Different factors influence the premium for each company.

| Insurance Company | Cost Structure Factors | Estimated Costs (Example) |

|---|---|---|

| Company A | Driving record, vehicle type, location | $1,200-$1,500 per year |

| Company B | Credit score, claims history, bundled policies | $1,000-$1,300 per year |

| Company C | Location, vehicle age, mileage | $1,400-$1,700 per year |

Note: These are example costs and may vary based on individual circumstances.

Evaluating Alternatives

Affording car insurance can be a significant financial hurdle for many individuals and families. Understanding alternative approaches to transportation and insurance coverage is crucial in navigating this challenge. Evaluating various options, from regional cost comparisons to alternative transportation methods, can lead to more sustainable and budget-friendly solutions.Evaluating different options for car insurance and transportation is vital when facing affordability issues.

This includes understanding regional variations in costs, insurance requirements, and the feasibility of self-insurance or limited coverage. Furthermore, exploring alternative transportation methods, like public transit or ride-sharing, can offer viable solutions for those unable to afford traditional car insurance.

Regional Cost Comparisons of Car Insurance

Car insurance premiums vary significantly across different regions and states. Factors such as driving habits, demographics, and local accident rates all contribute to these variations. Understanding these differences is crucial for making informed decisions. For example, states with higher accident rates or stricter regulations often have higher insurance premiums.

Differences in Car Insurance Requirements Across Jurisdictions

Insurance requirements differ considerably between jurisdictions. Some states mandate higher levels of coverage than others, and the types of coverage required also vary. For instance, some states may require liability coverage only, while others may mandate comprehensive and collision coverage. Understanding these distinctions is essential for determining the appropriate level of coverage in a specific area.

Potential for Self-Insuring or Purchasing Limited Coverage

Self-insurance, or carrying a higher deductible, can potentially lower insurance costs. However, it involves a significant risk. If an accident occurs, the individual or family is responsible for covering the costs not covered by their policy. Similarly, purchasing limited coverage can be a cost-effective solution, but it is vital to weigh the risks against the savings. For example, a person who rarely drives or primarily drives short distances might find limited liability coverage sufficient.

Alternative Transportation Options for Those Unable to Afford Car Insurance

For individuals who cannot afford car insurance, exploring alternative transportation options is essential. Public transportation systems, ride-sharing services, and cycling or walking are all viable alternatives. These options may not be suitable for everyone, but they can be valuable solutions for those who need to reduce their transportation costs.

Affordable Transportation Alternatives in Various Cities

Implementing sustainable transportation solutions is key to making mobility more affordable. This requires a city-by-city analysis to assess the suitability of different options.

- Public Transportation: Many cities have extensive public transportation networks, including buses, subways, and light rail. Analyzing routes, schedules, and fares is essential to determine their feasibility for daily commutes. For example, in New York City, the subway is a significant part of the transportation infrastructure, offering extensive coverage and affordability for many residents. In contrast, smaller towns might have limited or infrequent bus services.

- Ride-Sharing Services: Ride-sharing platforms like Uber and Lyft can offer affordable transportation options, especially for occasional or short-distance trips. However, costs can vary depending on demand and location. Comparing prices and travel times across different services can help find the best deal.

- Cycling and Walking: For shorter distances, cycling and walking can be cost-effective alternatives. However, factors like safety concerns, weather conditions, and distance to destinations need to be considered. This method is ideal for urban areas with well-maintained bike lanes and pedestrian walkways.

Analyzing Coverage Options: I Can’t Afford Car Insurance

Understanding the various car insurance coverage options is crucial for selecting a policy that adequately protects your financial interests while aligning with your budget. This section delves into the different tiers of coverage, highlighting the benefits and drawbacks of each, and provides a framework for making informed decisions based on individual needs and financial constraints.

Coverage Levels and Implications

Car insurance policies typically offer a spectrum of coverage levels, ranging from basic liability coverage to comprehensive policies. The chosen level directly impacts the premium amount and the degree of protection against potential losses.

- Liability Coverage: This fundamental coverage protects you if you’re at fault in an accident, covering the other party’s damages and medical expenses. However, it doesn’t cover your own vehicle or potential injuries. It’s the most basic form of protection, often required by law. Liability coverage usually comes in varying limits, such as $25,000 bodily injury per person, $50,000 bodily injury per accident, and $25,000 property damage.

Lower limits mean lower premiums but significantly reduced protection.

- Collision Coverage: This coverage compensates for damage to your vehicle resulting from a collision, regardless of who was at fault. This provides essential protection if your car is damaged in an accident where you are at fault or if you hit a stationary object. The cost of repair or replacement is covered, reducing financial burden.

- Comprehensive Coverage: This coverage extends beyond collisions, protecting your vehicle against various perils like vandalism, fire, theft, hail damage, or weather-related incidents. Comprehensive coverage offers peace of mind, as it covers damages not directly caused by a collision. It’s an important addition, especially in areas prone to high crime rates or severe weather.

- Uninsured/Underinsured Motorist Coverage: This coverage safeguards you if you’re involved in an accident with a driver who doesn’t have insurance or whose coverage limits are insufficient. It compensates for injuries and vehicle damage in such situations, filling a crucial gap in protection.

Selecting the Right Coverage

Choosing the appropriate coverage level hinges on individual circumstances, including the value of your vehicle, your driving record, and your financial situation. A thorough assessment of these factors allows for a customized approach to insurance selection.

- Vehicle Value: The higher the value of your vehicle, the more comprehensive coverage you might need for collision and comprehensive coverage. Consider the potential cost of repairs or replacement.

- Driving Record: Drivers with a history of accidents or violations might face higher premiums. A safe driving record often qualifies for discounted premiums.

- Financial Situation: Consider your financial capacity to absorb potential out-of-pocket costs. A higher deductible can lead to lower premiums, but you’ll have to pay a larger amount initially if a claim arises.

Comparing Policy Types

Different insurance companies offer various policy types, each with distinct features and benefits. Careful comparison is necessary to find the most suitable option for your needs.

- Bundled Policies: Combining car insurance with other policies, such as homeowners or renters insurance, often results in discounted premiums. Consider the potential savings when evaluating different policy options.

- Gap Insurance: This policy covers the difference between the value of your vehicle and what your insurance policy would cover in case of a total loss. It’s a valuable addition to consider if your vehicle has a high loan balance.

Potential Savings

Making informed choices about coverage can lead to significant cost savings. Lower deductibles and higher coverage limits may seem appealing, but they increase premiums. Careful consideration of risk tolerance and financial capacity is key to finding a balanced solution.

Insurance Policy Options

| Coverage Type | Premium (Example) | Deductible (Example) | Coverage Limits (Example) |

|---|---|---|---|

| Liability Only | $500 | $0 | $25,000 Bodily Injury / $25,000 Property Damage |

| Collision & Comprehensive | $1,200 | $500 | Actual Cash Value of Vehicle |

| Full Coverage (Collision, Comprehensive, Uninsured/Underinsured) | $1,500 | $1,000 | $100,000 Bodily Injury / $50,000 Property Damage |

Note: Premiums and deductibles are examples and may vary based on factors such as location, vehicle type, and driving history.

Practical Steps for Affordability

Reducing car insurance premiums requires a proactive and strategic approach. Understanding the various factors influencing premiums, such as driving history, vehicle type, and location, is crucial. Implementing practical steps to negotiate rates, compare quotes, and shop strategically can significantly impact the overall cost. This section Artikels actionable strategies for achieving more affordable car insurance.

Negotiating Car Insurance Premiums

Negotiation with insurance providers is a viable strategy for reducing premiums. This often involves presenting a compelling case that justifies a lower rate. Providing evidence of safe driving habits, such as a clean driving record and a history of accident-free years, can bolster your negotiation position. Highlighting any safety features installed on your vehicle, like anti-theft devices or advanced safety systems, might also sway the provider.

Furthermore, discussing discounts applicable to your situation can potentially lead to premium reductions. Ultimately, a clear understanding of your policy and the factors influencing it is paramount for successful negotiation.

Comparing Insurance Quotes from Different Providers

A systematic approach to comparing quotes from various insurance providers is essential. This involves gathering quotes from multiple insurers using online comparison tools or directly contacting providers. It’s crucial to ensure that all quotes are based on the same coverage parameters to facilitate accurate comparisons. Consider factors like deductibles, coverage limits, and policy add-ons when evaluating quotes.

Carefully reviewing each quote, noting specific details and terms, allows for a well-informed decision.

Shopping for Insurance During Specific Times of Year

Insurance shopping during specific times of the year, such as the new policy period or periods with lower demand, can lead to favorable rates. These periods often present opportunities for competitive pricing. Understanding these seasonal fluctuations in the insurance market can be advantageous. For instance, insurers might offer discounted rates during periods of low demand to attract new customers or retain existing ones.

This strategy requires awareness of market trends and timing for optimal results.

Bundling Insurance Policies for Potential Savings

Bundling insurance policies, such as combining auto, home, and life insurance with a single provider, can yield substantial savings. This approach leverages the insurer’s existing data and customer base to offer competitive rates. The synergistic effect of bundling policies often results in discounts, as insurers are incentivized to offer comprehensive packages. This approach often involves evaluating the potential savings against the comprehensive benefits of bundling different policies.

Insurance Discounts and Application

| Discount Type | Description | Application |

|---|---|---|

| Safe Driver Discounts | Based on a clean driving record. | Provide driving history to the insurer. |

| Multiple Policy Discounts | For bundling multiple insurance policies. | Combine policies with the same insurer. |

| Anti-theft Device Discounts | For vehicles with installed anti-theft systems. | Provide proof of installed security systems. |

| Defensive Driving Courses Discounts | For completing defensive driving courses. | Provide certificate of completion. |

| Good Student Discounts | For students with good academic records. | Provide academic transcripts. |

| Homeowner Discounts | For homeowners with certain insurance packages. | Provide details about your home insurance policy. |

Applying for these discounts often requires providing supporting documentation, such as driving records, certificates, or proof of insurance. A clear understanding of the requirements for each discount is crucial for successful application.

Illustrative Scenarios

Affordability of car insurance is a complex issue, often exacerbated by fluctuating premiums, rising living costs, and individual financial circumstances. Understanding real-world scenarios provides valuable insight into the challenges faced by individuals and highlights potential solutions. These scenarios demonstrate the impact of various factors on insurance costs and explore strategies for managing the financial burden.Illustrative scenarios help to contextualize the difficulties associated with obtaining and maintaining adequate car insurance coverage.

They also provide concrete examples of how individuals can explore various options, from negotiating with providers to seeking government assistance.

Scenario 1: Struggling to Afford Coverage

A single parent, Sarah, works a part-time job as a cashier earning $1,500 per month. Her monthly expenses include rent ($800), utilities ($150), groceries ($250), transportation ($100), and childcare ($200). Her car, a five-year-old sedan, is essential for her work and childcare duties. She needs comprehensive coverage to protect her investment and her family’s safety. However, a quote for a basic policy exceeds 25% of her disposable income.

This demonstrates how a low income can make even basic coverage unattainable.

Scenario 2: Finding Affordable Insurance

John, a recent college graduate with a new car, faces high premiums due to his young age and driving record. He researches different insurance providers, comparing coverage options and premiums. He learns about discounts available for good students and safe drivers. He also explores usage-based insurance programs that offer lower premiums for safe driving habits. By comparing quotes from multiple providers, selecting appropriate coverage, and utilizing available discounts, John identifies an insurance plan that aligns with his budget.

Scenario 3: Reducing Car Insurance Costs

Maria, a responsible driver with a clean driving record, decides to take proactive steps to lower her insurance costs. She upgrades her vehicle’s anti-theft features, installs a telematics device to monitor her driving habits, and maintains her vehicle’s excellent condition. These actions demonstrate how a proactive approach to driving and car maintenance can significantly impact insurance premiums. She also considers a higher deductible to reduce her monthly premium.

Scenario 4: Government Assistance Programs

David, a low-income individual, qualifies for a state-sponsored program that subsidizes car insurance premiums. This program provides a significant reduction in his insurance costs, enabling him to afford the necessary coverage. By utilizing these programs, individuals can significantly lower their financial burden while ensuring their vehicle and themselves are protected. Many such programs are available through state and local agencies.

Scenario 5: Financial Impact of Insurance Choices

| Insurance Choice | Monthly Premium | Total Annual Cost | Impact on Budget (Example) |

|---|---|---|---|

| Basic Liability | $150 | $1800 | Affordable, but limited protection |

| Comprehensive Coverage | $250 | $3000 | Provides wider protection but increases budget pressure |

| Enhanced Coverage (with discounts) | $200 | $2400 | Balanced protection and affordability |

This table demonstrates the financial implications of different insurance choices. It illustrates how the cost of coverage can vary significantly, impacting a budget, and the trade-offs involved in different coverage options. The impact on a budget is an important consideration when choosing insurance, as highlighted in the example.

Conclusive Thoughts

In conclusion, finding affordable car insurance when facing financial constraints requires careful consideration of various factors. This guide has Artikeld several solutions, including cost-reduction strategies, government assistance, and alternative transportation options. By understanding the available options and taking practical steps, individuals can potentially secure suitable and affordable car insurance coverage. Remember to prioritize your financial well-being and seek professional advice when necessary.

Helpful Answers

What are some common ways to reduce car insurance premiums?

Improving your credit score, bundling policies, and taking defensive driving courses are common ways to potentially reduce premiums.

Are there government programs to help with car insurance costs?

Yes, some states and localities offer assistance programs for low-income individuals, so it’s worth researching options in your area.

What are some alternatives to car insurance if I can’t afford it?

Alternative transportation options like public transportation or ride-sharing services might be considered, although legal ramifications may exist.

How can I compare car insurance quotes from different providers?

Use online comparison tools or contact insurance providers directly to get multiple quotes and compare costs.