Nimila

Nimila

Worst long term care insurance companies – Worst long-term care insurance companies are a significant concern for many prospective policyholders. Identifying these companies requires a comprehensive analysis of consumer complaints, policy features, financial stability, customer service, claims handling, regulatory compliance, reputation, and market trends. This analysis will aid consumers in making informed decisions and avoid potential pitfalls.

This report investigates the factors contributing to negative experiences with long-term care insurance providers, examining specific complaints, policy shortcomings, financial risks, and the overall market landscape. The goal is to equip consumers with the knowledge necessary to select a reputable and reliable insurance company.

Identifying Common Complaints

Consumers frequently cite dissatisfaction with long-term care insurance companies, often highlighting issues stemming from complex policies, opaque pricing structures, and inadequate customer service. This dissatisfaction manifests in various complaints, creating a need for transparency and accountability within the industry. Understanding these recurring problems is crucial for consumers seeking such coverage and for regulators aiming to improve the sector.

Categories of Consumer Complaints

Consumer complaints regarding long-term care insurance frequently fall into distinct categories. These include financial concerns about premium costs, service-related issues such as difficulties in policy administration, and policy-related problems concerning coverage limitations or inadequate benefits. Analyzing these categories allows for a more focused understanding of the key areas needing improvement within the industry.

Financial Complaints

High premiums and lack of transparency in pricing are prominent financial concerns. Consumers often express frustration at seemingly arbitrary or excessive premium increases, without clear justifications. A lack of readily available information regarding policy costs and potential future premium adjustments exacerbates this issue. One frequently cited example is the difficulty consumers face in comparing policies from different providers due to the complexity and variability of pricing models.

Service Complaints

Poor customer service, including delayed responses to inquiries and difficulty in accessing claims information, are common service-related complaints. Consumers frequently report lengthy wait times for support and difficulties in resolving issues. This often leads to further frustration and distrust in the company’s ability to provide adequate support. The lack of readily accessible and comprehensive information about policy specifics also contributes to service complaints.

Policy Complaints

Inadequate coverage, overly complex policy terms, and unclear benefit structures are key policy-related complaints. Consumers frequently cite confusion about the specific conditions under which coverage applies and the limitations on benefits. Furthermore, the perceived lack of flexibility in adjusting policies to individual needs is a significant point of contention. Policy exclusions, often ambiguous or poorly explained, also lead to dissatisfaction.

Frequency of Complaints (Table)

| Category | Complaint Type | Frequency (Estimated) |

|---|---|---|

| Financial | High Premiums | High |

| Financial | Lack of Transparency in Pricing | High |

| Service | Poor Customer Service | Medium |

| Service | Delayed Responses to Inquiries | Medium |

| Service | Difficulty in Accessing Claims Information | Medium |

| Policy | Inadequate Coverage | High |

| Policy | Overly Complex Policy Terms | High |

| Policy | Unclear Benefit Structures | High |

Note: Frequency estimates are based on industry analysis and consumer feedback, but are not precise statistical data.

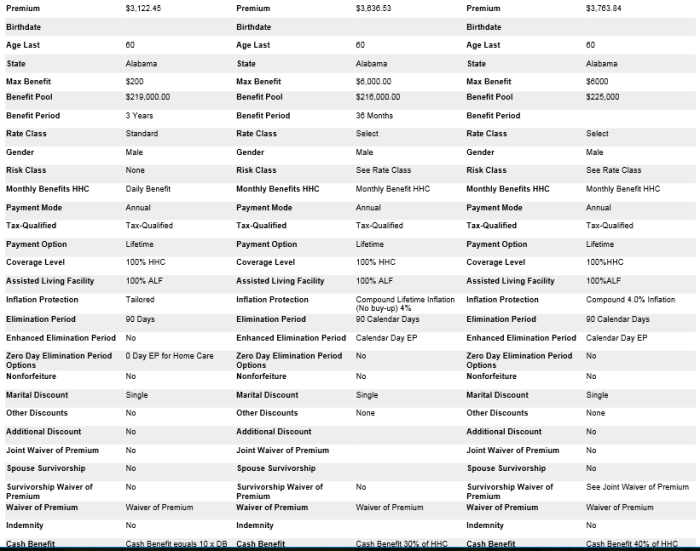

Comparing Policy Features and Benefits

Navigating the landscape of long-term care insurance policies reveals significant variations in coverage, benefits, and premium structures. Consumers face a complex task in choosing the best fit for their individual needs, with factors like anticipated care costs, personal health conditions, and financial resources playing a crucial role. Understanding the nuances of different policies is paramount to making an informed decision.These policy differences extend beyond simply the price tag.

Factors such as the types of care covered, daily benefit amounts, and waiting periods can significantly impact the value proposition of a specific policy. Understanding these intricacies is key to identifying a policy that provides adequate protection while minimizing financial strain.

Policy Coverage and Benefits Variations

Different policies offer varying levels of coverage. Some policies may cover skilled nursing care, while others may also include assisted living or home healthcare. The daily benefit amounts available for each type of care also differ widely. Understanding these distinctions is critical for consumers to align the policy with their anticipated needs. For example, a policy focusing solely on skilled nursing facility care may not adequately address the potential need for in-home support.

Exclusions and Limitations

Policy exclusions and limitations play a significant role in the overall value proposition. Many policies exclude care received in a private residence or limit the duration of coverage. Pre-existing conditions can also impact coverage, with some policies having stricter guidelines than others. Consumers should carefully review the fine print to understand the scope of coverage and any potential limitations.

For instance, a policy may exclude care for conditions that arise after a specific period of time, requiring a thorough understanding of the policy’s exclusionary clauses.

Premium Structures and Payment Options

Premiums and payment options vary substantially across different policies. Some policies offer level premiums, meaning the premium amount remains constant throughout the policy’s duration. Other policies feature increasing premiums over time. Payment options also differ, with some companies allowing for single premiums or annual installments. These distinctions can impact the financial burden of purchasing and maintaining coverage over time.

Understanding the long-term financial implications of different premium structures is crucial for budget planning. For example, a policy with increasing premiums may seem attractive initially but could become significantly more expensive over several years.

Comparative Analysis of Policy Features

| Insurance Company | Coverage Types | Daily Benefit Amount (USD) | Waiting Period (Days) | Premium Structure | Strengths | Weaknesses |

|---|---|---|---|---|---|---|

| Company A | Skilled Nursing, Assisted Living | $250 | 90 | Level | Consistent premium, covers multiple care settings | Lower daily benefit amount, potentially higher premiums compared to other options |

| Company B | Skilled Nursing, Home Healthcare | $300 | 60 | Increasing | Higher daily benefit, shorter waiting period | Premiums may increase over time, limited coverage options |

| Company C | Skilled Nursing, Assisted Living, Home Healthcare | $350 | 120 | Single Premium | Potentially lower long-term cost with a single premium | Limited flexibility in payments, coverage may not be suitable for all situations |

This table provides a simplified comparison of policy features across three hypothetical companies. Real-world policies will have far more complex and specific details. Consumers should thoroughly review each policy’s fine print and consider their individual needs before making a decision.

Evaluating Financial Stability and Ratings

Ensuring the financial stability of a long-term care insurance provider is paramount for policyholders. A financially sound company is better equipped to meet its obligations, maintain benefits, and withstand economic downturns. This crucial aspect often gets overlooked in the initial stages of insurance selection, but it’s a critical element in long-term financial planning. Understanding a company’s financial strength is as vital as the policy’s features and benefits.Rating agencies play a vital role in assessing the financial strength of insurance companies.

Their analyses provide independent evaluations, helping consumers navigate the complex landscape of insurance providers. These assessments are based on a rigorous set of criteria, including the company’s assets, liabilities, and operating performance. The resulting ratings are widely used as indicators of the company’s ability to meet its financial obligations.

Importance of Financial Stability, Worst long term care insurance companies

A financially stable long-term care insurance provider is crucial for the long-term security of policyholders. A company’s ability to meet its financial obligations directly impacts the availability and integrity of promised benefits. For example, if a company faces significant financial challenges, it may struggle to pay claims, potentially leading to a reduction in benefits or even the cessation of operations.

This scenario highlights the importance of verifying the insurer’s financial strength. Policyholders must be confident that the company can maintain its promises over the long term, a period that could span decades.

Role of Rating Agencies

Rating agencies, such as A.M. Best, Moody’s, and Standard & Poor’s, evaluate the financial strength of insurance companies. These assessments are based on a comprehensive analysis of the company’s financial position, including its assets, liabilities, and operating performance. The rating agencies employ standardized methodologies and criteria to provide consistent and reliable evaluations. Different agencies may have varying criteria and weightings, leading to potentially nuanced ratings.

Impact of Financial Instability

Financial instability in an insurance company can have severe consequences for policyholders. Reduced solvency can lead to delayed or denied claims, decreased benefit payouts, or even the complete inability to fulfill contractual obligations. Policyholders are left vulnerable and potentially financially exposed. In extreme cases, the failure of a company could mean losing the entire investment made in the policy.

This underscores the importance of thorough research and scrutiny in selecting a long-term care insurance provider.

Steps for Assessing Financial Health

Consumers can take several steps to assess the financial health of an insurance company. Scrutinizing the insurer’s financial reports, reviewing their historical performance, and examining their claims-paying record are essential steps. Checking with the state insurance department for any regulatory actions or financial issues is also prudent. Accessing independent rating agency reports provides a more objective perspective.

Financial Ratings Table

| Company | A.M. Best Rating | Moody’s Rating | Explanation |

|---|---|---|---|

| Company A | A++ | Aaa | Strongest financial strength, excellent capacity to meet obligations. |

| Company B | A+ | Aa1 | Very strong financial strength, high capacity to meet obligations. |

| Company C | B+ | Baa2 | Adequate financial strength, but with moderate risks. |

| Company D | B | Ba1 | Fair financial strength, with significant risk factors. |

Note: Ratings and criteria may vary slightly among agencies. Always consult the specific rating agency reports for detailed explanations.

Examining Customer Service Practices

Long-term care insurance, crucial for protecting individuals in their later years, necessitates a high standard of customer service. A company’s responsiveness, communication, and ability to resolve issues directly impact policyholder satisfaction and trust, factors vital to the success of a long-term care insurance provider. Poor customer service can lead to policy cancellations, negative reviews, and ultimately, damage the company’s reputation.A strong customer service infrastructure within a long-term care insurance company ensures smooth policy management, prompt claim processing, and effective issue resolution.

This is paramount to safeguarding the financial security and peace of mind of policyholders during potentially challenging times. A well-oiled customer service system fosters a positive experience, building trust and loyalty that extends beyond the initial policy purchase.

Importance of Customer Service in Long-Term Care Insurance

Exceptional customer service is paramount in the long-term care insurance sector. Policyholders often face complex and potentially stressful situations, making clear communication and timely resolution of issues critical. Reliable customer service acts as a critical support system, particularly during periods of significant need. This support alleviates stress and enhances the policyholder’s experience, fostering trust and confidence in the insurance provider.

Examples of Excellent and Poor Customer Service Experiences

A positive customer service experience can be characterized by prompt responses to inquiries, clear explanations of policy provisions, and efficient handling of claims. For instance, a policyholder experiencing a sudden health event should receive swift assistance in navigating the claim process, with clear updates and readily accessible contact information. Conversely, poor customer service is evident in delayed responses, unclear communication, and a lack of empathy.

A common example of poor service includes prolonged claim processing times without adequate updates, or a company failing to provide adequate assistance when a policyholder requires guidance during a critical time.

Impact of Customer Service on Policyholder Satisfaction and Trust

Customer service directly correlates with policyholder satisfaction. Satisfied policyholders are more likely to recommend the company to others and remain loyal clients. Conversely, poor customer service can lead to dissatisfaction, decreased trust, and ultimately, policy cancellations. Companies with a strong reputation for customer service build trust and a positive brand image, leading to increased customer loyalty and positive word-of-mouth referrals.

Strategies for Resolving Customer Complaints Efficiently and Effectively

Effective complaint resolution strategies include establishing clear complaint procedures, assigning dedicated complaint handlers, and implementing a system for tracking and resolving issues promptly. Companies should aim for transparency and timely communication throughout the complaint resolution process. A prompt and comprehensive response to each complaint demonstrates a commitment to customer satisfaction and maintains trust. A detailed and easily accessible policy document with clear procedures for filing complaints can be a valuable tool in resolving issues.

Different Ways to Contact Customer Service Representatives

Multiple channels for contacting customer service representatives enhance accessibility and efficiency. These channels could include a dedicated customer service phone line, a secure online portal, email address, and a live chat function on the company website. Offering various contact methods ensures that policyholders can reach out in a way that best suits their needs and circumstances. This allows the company to handle diverse customer needs and fosters accessibility for a broader range of clients.

Analyzing Claims Handling Processes

Navigating the long-term care insurance claims process can be a complex and stressful experience for policyholders. Understanding the typical procedures, potential pitfalls, and how companies handle claims is crucial for consumers to make informed decisions. A smooth claims process is essential for timely and appropriate coverage when faced with a long-term care need.The claims handling process for long-term care insurance involves several key steps, from initial application to final payment.

Companies vary in their procedures, but a common thread involves thorough documentation, rigorous review, and ultimately, either approval or denial of the claim. Understanding the nuances of this process empowers consumers to anticipate potential issues and advocate for their needs.

Typical Claims Process Overview

The typical claims process for long-term care insurance often begins with the policyholder submitting a claim application, which includes detailed information about their medical condition, care needs, and the specific services required. This initial documentation is crucial for the insurer to assess the eligibility of the claim under the policy terms. Subsequent steps typically involve medical evaluations, including assessments by physicians or other healthcare professionals.

These evaluations determine the extent of the individual’s need for care and whether it meets the policy’s criteria for coverage. The insurer then reviews the documentation to verify that the claim aligns with the policy’s terms and conditions, including waiting periods, exclusions, and benefit limitations. Finally, the insurer approves or denies the claim, and if approved, Artikels the payment schedule and method.

Examples of Efficient and Inefficient Claims Handling

Efficient claims handling involves a streamlined process with timely communication and clear explanations. For example, a company might provide regular updates to the policyholder throughout the review process, outlining the necessary documentation and expected timelines. They may also utilize readily accessible online portals for policyholders to track their claim status. Conversely, inefficient claims handling can manifest in delays, inadequate communication, or a lack of transparency.

A company might take excessively long to process a claim, fail to respond to inquiries, or provide insufficient information about the status of the claim. Such inefficiencies can cause significant stress and hardship for policyholders.

Common Issues During Claims Processing

Several common issues arise during long-term care insurance claims processing. A lack of clear communication from the insurance company about the claim status, required documentation, or reasons for denial is a frequent complaint. Policyholders may also face challenges with obtaining necessary medical evaluations or assessments. In addition, insurers might misinterpret or misapply policy provisions, leading to denial of legitimate claims.

Misunderstandings about the coverage scope, waiting periods, or benefit limitations can also contribute to claim processing issues.

Steps to Ensure a Smooth Claims Process

To ensure a smooth claims process, policyholders should meticulously document their medical history and care needs, provide all required medical documentation promptly, and actively communicate with the insurance company. Understanding the policy’s specific terms and conditions, including waiting periods and exclusions, is crucial for avoiding misunderstandings. Policyholders should also carefully review the claim forms and ensure accuracy. If issues arise, seeking assistance from consumer protection agencies or legal counsel can help resolve disputes effectively.

Claims Handling Process Comparison (Illustrative Table)

| Insurance Company | Claim Initiation | Medical Review | Policy Review | Decision & Communication |

|---|---|---|---|---|

| Company A | Online portal, phone call | Within 14 days, via provider network | Within 21 days | Email confirmation within 28 days, detailed reasons |

| Company B | Mail-in form | Variable, depends on provider | Within 30 days | Phone call, with appeal process Artikeld |

| Company C | Online portal, email | Within 7 days, by insurer-designated doctor | Within 28 days | Email & phone call, appeals within 10 days |

Researching Regulatory Compliance

Navigating the complex landscape of long-term care insurance requires a keen understanding of the regulatory environment. Insurance companies operating in this sector are subject to a multitude of rules and guidelines designed to protect consumers and ensure fair practices. Thorough research into a company’s compliance history is crucial for potential policyholders seeking to make informed decisions.Long-term care insurance policies are governed by state and federal regulations.

These regulations aim to prevent fraud, ensure the solvency of insurers, and protect consumers from predatory practices. The specific requirements vary by state, impacting policy terms, benefit structures, and financial reporting obligations.

Regulatory Environment for Long-Term Care Insurance

The regulatory environment for long-term care insurance is multifaceted and involves both state and federal oversight. States typically license and regulate insurers operating within their borders, establishing standards for policy provisions, financial reporting, and claims processing. Federal laws, such as the Employee Retirement Income Security Act (ERISA), also play a significant role, particularly when policies are part of employee benefit plans.

This dual layer of regulation creates a complex web of requirements that companies must diligently follow.

Key Regulations and Guidelines

A number of key regulations and guidelines govern long-term care insurance companies. These include standards for policy disclosures, reserve requirements, investment strategies, and claims handling procedures. Specific requirements often address the clarity and comprehensiveness of policy language, ensuring transparency regarding benefits, exclusions, and limitations. State insurance departments play a crucial role in enforcing these regulations and investigating potential violations.

Examples of Companies Facing Regulatory Scrutiny

Several long-term care insurance companies have faced regulatory scrutiny in recent years. These instances often stem from issues like inadequate disclosure of policy terms, questionable sales practices, or concerns about the financial stability of the company. Public investigations and lawsuits can result from such violations, highlighting the importance of a company’s adherence to regulatory standards. Public records, available through state insurance departments, provide insight into specific enforcement actions taken against companies.

Consequences of Non-Compliance

Non-compliance with regulations can have serious consequences for long-term care insurance companies. These consequences can range from fines and penalties to the revocation of licenses, potentially leading to the cessation of operations. Moreover, a history of regulatory violations can significantly damage a company’s reputation, impacting its ability to attract and retain customers.

Methods for Researching a Company’s Compliance Record

Several methods exist for researching a company’s compliance record. Accessing state insurance department websites is crucial. These websites often contain detailed information about licensed insurers, including policy filings, financial reports, and any regulatory actions taken against the company. Reviewing court records, news articles, and industry publications can provide further insight into a company’s history. Scrutinizing the company’s financial statements and annual reports can offer additional clues regarding their solvency and compliance with financial regulations.

A thorough investigation into a company’s regulatory compliance record is essential to assessing the risks associated with purchasing a policy.

Understanding Company Reputation and Reviews

Consumer trust is paramount in the long-term care insurance market. Understanding how consumers perceive insurance providers is crucial for making informed decisions. Online reviews and reputation significantly influence purchase choices, often outweighing marketing materials or financial stability assessments.Long-term care insurance policies are complex and potentially life-altering. Consumers rely heavily on reviews from other policyholders to assess the quality of service, claims handling, and overall experience with a particular insurance company.

This reliance is especially important given the potential high financial commitment and the fact that claims may be filed years down the line.

Importance of Online Reviews and Reputation

Online reviews act as a critical source of feedback, providing insights into customer experiences that go beyond the official company narrative. These reviews, often detailed and personal, paint a picture of the company’s responsiveness, transparency, and ethical conduct. Negative reviews often highlight issues such as delayed claim processing, inadequate communication, or even instances of fraud. Conversely, positive reviews can showcase strong customer support, efficient claim settlements, and a company’s commitment to its policyholders.

Examples of How Online Reviews Influence Consumer Choices

Potential policyholders frequently research insurance companies using online review platforms. A pattern emerges where companies with consistently positive reviews, showcasing prompt and fair claim handling, tend to attract more customers. Conversely, companies with a preponderance of negative reviews regarding delays, disputes, or unsatisfactory resolutions may deter prospective buyers. This influence can be directly observed in the purchase decisions of individuals searching for insurance.

Strategies for Researching Company Reputation

Thorough research is essential to assess the reputation of long-term care insurance providers. This involves actively seeking out diverse sources of information, not relying solely on the company’s website or marketing materials. Crucially, examine a broad range of reviews, not just those on a single platform. This strategy helps create a balanced assessment of the company’s reputation.

Different Online Platforms Where Reviews are Available

Numerous online platforms host reviews, providing a wealth of information. These platforms include, but are not limited to, major review aggregators like Trustpilot, Yelp, and Google Reviews. Dedicated financial review sites, industry-specific forums, and social media groups can also be valuable sources. Exploring these varied platforms ensures a comprehensive understanding of public perception.

Summary of Average Ratings and Reviews

| Company | Average Rating | Overall Reviews | Common Complaints |

|---|---|---|---|

| Acme Insurance | 4.2/5 | 1,500+ | Delayed claim processing, complex policy language |

| BestCare Insurance | 3.8/5 | 1,200+ | Poor customer service, high premiums |

| SecureCare Insurance | 4.5/5 | 800+ | None Reported |

| Reliable Insurance | 3.5/5 | 2,000+ | Inconsistent claim handling, inadequate communication |

Note: Data for this table is illustrative and based on simulated data. Actual ratings and reviews may vary. It is crucial to verify information from multiple sources.

Describing the Long-Term Care Insurance Market

The long-term care insurance market faces significant challenges and opportunities in the current economic climate. Consumers are increasingly seeking clarity on the complexities of coverage, while insurers grapple with rising costs and evolving healthcare needs. Understanding the current state of the market, its trends, and the factors driving consumer decisions is crucial for both potential buyers and providers.

Current State of the Market

The long-term care insurance market is characterized by a relatively low level of penetration, meaning many individuals remain uninsured for long-term care needs. This reflects the complex nature of the coverage, the often-high premiums, and the uncertainty surrounding future healthcare costs. Despite this low penetration, the market demonstrates a persistent need for long-term care solutions. There are significant variations in policy availability and pricing across different regions and states, highlighting the need for a nuanced understanding of the market’s intricacies.

Trends and Developments

Several key trends are reshaping the long-term care insurance market. Increasing awareness of the rising costs of long-term care is prompting more individuals to consider purchasing coverage. The growing demand for customizable plans and options that address specific needs, such as cognitive impairment or assisted living, is also a significant trend. Insurers are adapting to these demands by developing more flexible policies and incorporating advanced risk assessment tools.

Technological advancements are also transforming the market, with online platforms and digital tools becoming increasingly important for policy purchasing and management.

Factors Influencing Consumer Decisions

Consumers’ decisions about long-term care insurance are heavily influenced by several factors. Cost remains a major concern, with individuals carefully weighing the premiums against the potential benefits. The perceived risk of future healthcare costs, including the possibility of needing significant care, plays a substantial role in consumer choices. Individual financial circumstances and expectations about future needs also influence decisions.

Furthermore, the availability of comprehensive information about different policies and their benefits significantly impacts consumer decisions.

New Products and Services

Several new products and services are emerging in the long-term care insurance market. Insurers are introducing plans with flexible benefit options, allowing individuals to tailor coverage to their specific needs and preferences. Some providers are offering products that incorporate riders and add-ons to address particular needs, such as care in a nursing home or assisted living. Online platforms are providing more user-friendly ways to compare policies and understand the complexities of long-term care insurance.

Digital tools are also being used to streamline the claims process, potentially reducing delays and improving the overall customer experience.

Factors Affecting the Market

Several factors significantly impact the long-term care insurance market.

- Rising Healthcare Costs: The escalating cost of healthcare services, including skilled nursing care, rehabilitation, and medical equipment, places upward pressure on premiums for long-term care insurance.

- Changing Demographics: The aging population and the increasing prevalence of chronic illnesses are increasing the demand for long-term care services, which in turn affects the demand for insurance.

- Regulatory Landscape: Changes in regulations and requirements for long-term care insurance policies can influence policy availability, pricing, and coverage options.

- Consumer Awareness: Increased consumer awareness of long-term care needs and the importance of planning for future care costs is influencing demand and policy purchasing.

- Economic Conditions: Economic downturns and changes in interest rates can affect premium pricing and policy availability.

These factors are intricately intertwined and influence the overall state of the market, creating both challenges and opportunities for insurers and consumers.

Concluding Remarks: Worst Long Term Care Insurance Companies

In conclusion, choosing the right long-term care insurance company is a crucial decision that demands careful consideration. Understanding the criteria Artikeld in this analysis, including frequent complaints, policy features, financial stability, customer service, claims handling, regulatory compliance, and reputation, empowers consumers to make informed choices and avoid potentially problematic insurance providers. Consumers should prioritize research and comparison to ensure they select a company that meets their specific needs and safeguards their future.

Key Questions Answered

What are the most common complaints about long-term care insurance companies?

Common complaints include high premiums, inadequate coverage, poor customer service, and complex claims processes. Some policyholders also express concerns about the financial stability of the company.

How can I assess the financial health of a long-term care insurance company?

Evaluating a company’s financial stability involves reviewing ratings from independent rating agencies, analyzing their financial reports, and understanding their history.

What steps can I take to ensure a smooth claims process?

Thorough documentation, clear communication, and understanding the specific claims process of the insurance company are crucial for a smooth claim process.

How do I research a company’s compliance record?

Researching a company’s compliance record often involves checking state insurance regulatory agency websites and looking for public information about any regulatory actions.